-

STR Commentary on U.S. Performance for October 2023

Top-Line Metrics (percentage change from October 2022):

- Occupancy: 65.8% (-1.8%)

- ADR: $161.56 (+3.0%)

- RevPAR: $106.38 (+1.2%)

Bottom-Line Metrics (percentage change from October 2023):

- TRevPAR: $240.74 (+4.0%)

- GOPPAR: $97.45 (+3.7%)

- EBIDTA PAR: $69.60 (-1.2%)

- LPAR: $74.48 (+5.9%)

Key points

- RevPAR growth decelerated on falling demand due mostly to a calendar shift.

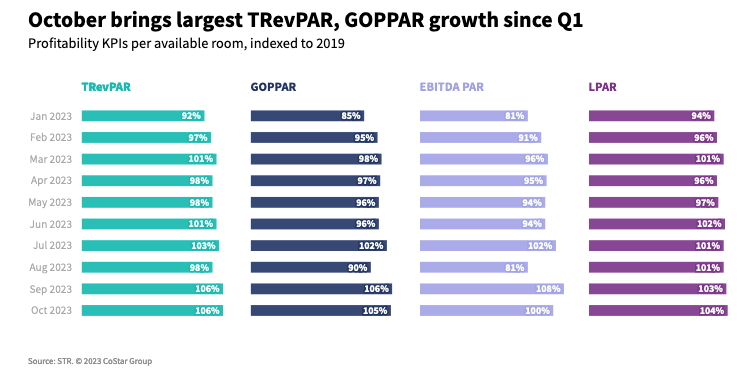

- Both TRevPAR and GOPPAR showed the highest year-over-year growth since March.

- Group demand in Luxury and Upper Upscale class hotels was the highest for any single month since October 2018.

- Upper Upscale chains are continuing to lead the growth in revenues and profits, with better than 16% GOPPAR growth through October year to date. Luxury chains are the only scale to show GOPPAR declines this year.

- Room labor costs (per occupied room) are up 7%, the second highest labor cost increase behind F&B labor (+9%). Overall labor costs POR are up approximately 7.5%.

- Catering and banquet revenues are up 20% from last year.

- The volume of rooms under construction increased from a month prior but remained down versus a year ago.

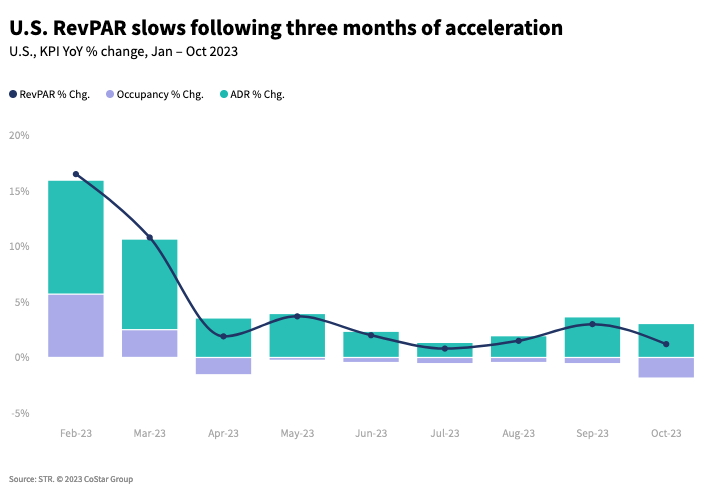

Year-over-year growth in RevPAR softened to +1.2% after coming in at +3% a month prior. Demand dropped 1.2%, which was the largest decrease since April. Like April, a calendar shift was largely responsible for the fall. Compared to last year, this October included one less Saturday (from five last year to four this year) and the gain of Halloween Tuesday. The latter was insufficient to replace Saturday’s demand given the Halloween impact. To illustrate the impact of the calendar shift, demand for the 28 days ending 28 October was nearly flat (-0.2%).

Year to date, RevPAR decreased from +6.1% a month prior to +5.5%. The RevPAR downward trend is in line with STR’s November forecast update, which shows full year RevPAR growth of +4.8%. Despite the ups and downs of the year, hotelier sentiment for 2024 continues to be positive, especially for group and business demand. Our forecast with Tourism Economics reflects that optimism as 2024 RevPAR is predicted to grow 4.1%, unchanged from the previous forecast.

October TRevPAR and GOPPAR, however, showed the highest year-over-year growth since March.

Chain scale performance

The three top chain scales (Luxury through Upscale) have seen demand growth in every month of 2023. With relatively low supply growth, these three chains have also reported occupancy growth as well during the last four consecutive months. However, Luxury continued to report ADR decreases, although it was almost flat in October.

The remaining three chain scales and Independents showed meaningful declines in occupancy year over year, especially the Economy chain hotels, which decreased 4.8% from October 2022.

Segmentation

For the first time since May 2023, growth in Luxury and Upper Upscale demand outpaced transient. October Group demand exceeded both 2022 and 2019 levels, making it the highest level in the metric since October 2018. Transient demand slightly edged past 2022 but remained behind 2019. Transient weekend and shoulder day occupancy maintained a steady year-over-year increase. Group occupancy was strong during the shoulder and weekday periods but remained flat on the weekend, likely due to the loss of a Saturday compared with October 2022.

Markets

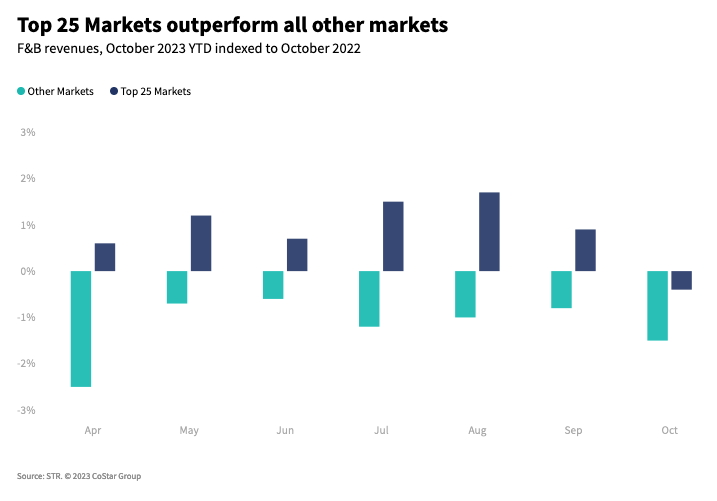

Top 25 Market demand fell less than the rest of the country, and ADR grew faster versus those remaining markets. Of course, occupancy was down, but the gap in the level to the remaining markets widened after narrowing in the summer. Weekday (Monday-Wednesday) occupancy was solid at 71%, up from 69.4% in September and well ahead of the 61.4% seen elsewhere. What was even more impressive was the 80.2% weekend occupancy, which tied the level seen in the heart of summer (July). While impressive, last October, Top 25 occupancy was 80.7%.

Pipeline

The number of rooms under construction increased 6.7% from September. The largest gain was seen in unaffiliated projects, which showed a 25% month-over-month increase. However, the number of rooms under construction still trails 2022 (-1.3%) with many projects in a holding pattern as witnessed by the year-over-year gain in rooms in final planning rooms (+32%).

This article originally appeared on STR.