-

Weekly Global Hotel Performance Trends from STR: 5-11 November 2023

Global Performance

Global occupancy, excluding the U.S., also improved following a year-over-year decline the week before. Occupancy increased 3.9ppts WoW to 68%. Year over year, occupancy also continued to improve at a much faster rate than the U.S., increasing 7ppts compared to the same week last year. Weekly global ADR increased 10% YoY, keeping RevPAR growth in double figures (+17.6%).

RevPAR among the top 10 countries (based on supply) increased 24.2% YoY on an 11.1% gain on ADR. Occupancy rose 7.4ppts. Every country saw RevPAR growth except Mexico, which declined on falling ADR. Five of the top 10 reported double-digit increases, led by China, Japan, Spain, Germany, and Indonesia, with most of those countries seeing equal gains in both occupancy and ADR. Japan and Spain were the exception as ADR accounted for most of the RevPAR growth.

For the past six weeks, China has contributed an average of five percentage points to the growth in global RevPAR via rising occupancy. This week, China’s occupancy increased by 15ppts with ADR gaining 23.3% and resulting in 61.3% RevPAR growth. While its ADR growth was impressive, global ADR growth rises when China is excluded.

RevPAR in Mexico has fallen for more than 20 weeks, mostly on decreasing ADR. Most of the ADR decrease is coming from Mexican Caribbean hotels, which have seen steep decreases since April. Over the past three weeks, the declines have lessened from double-digit ones to -1% this most recent week. We believe this is also due to the rebalancing of the industry as high-income travelers have taken their stays to other parts of the world that were inaccessible during the pandemic.

Outside of the top 10, performance was led by these countries:

- Americas: El Salvador, 84.5% (+12.2ppts YoY), which also posted the highest occupancy of any country in the world.

- Asia Pacific: French Polynesia, 81.1% (+1.5ppts YoY)

- Europe: Serbia, 80.6% (+7.5ppts YoY).

- Middle East & Africa: United Arab Emirates, 83.4% (+1.5ppts YoY)

Weekly results driven by midweek travel, Top 25 Markets, top chain scales and strong group performance

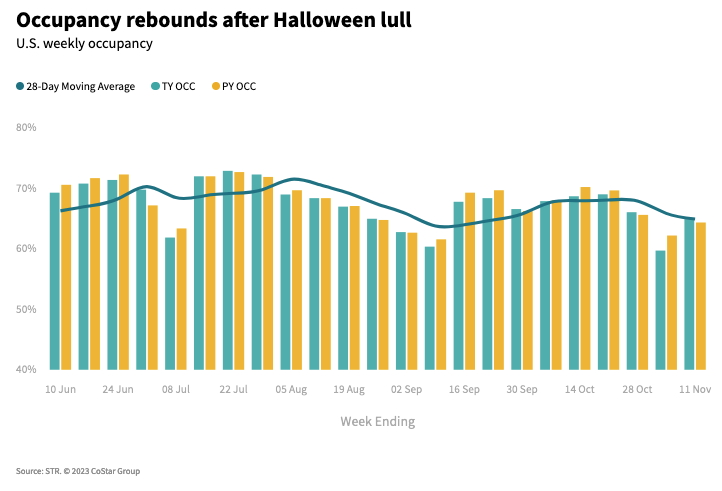

The U.S. hotel industry reemerged from the Halloween induced slowdown with occupancy increasing to 64.8%, up 5.2 percentage points (ppts) from the prior week and 0.5ppts year over year (YoY). Average daily rate (ADR) increased 4.0% YoY, restarting the 3%-plus growth streak that halted the previous week. Prior to that decline, ADR had grown 3% or more for six straight weeks. Revenue per available room (RevPAR) improved 4.9% YoY, which represented the largest weekly increase since early October.

Weekday (Monday – Wednesday) travel, likely business and group, was largely responsible for the week’s strong performance. Midweek RevPAR increased 9.2% YoY, the second largest increase for that day type since early May, thanks to occupancy increasing 2.1ppts to 64.9% and ADR rising 5.6%. Shoulder days (Sunday and Thursday) also showed RevPAR growth (+3.8%) driven by ADR (+4.1%), while weekend RevPAR was essentially flat (+0.9%) due to an occupancy decline (-1.1%) and modest ADR growth (+2.4%). Despite the drop, weekend occupancy remained above 70% for an 11th consecutive week.

The Top 25 Markets took the week’s improved performance to the next level with weekday RevPAR up 11.9%, the second largest RevPAR gain since early July. That gain came as occupancy increased 3.5ppts to 72.9% and ADR grew 6.5%. Shoulder RevPAR followed, increasing 6.7% with ADR up 4.9% and occupancy up 1.1ppts, while weekends were soft with RevPAR up 2.9% driven by both occupancy (+1.0ppts) and ADR (+1.6%) gains. Weekend occupancy returned to a level above 80% after two weeks in the mid-70s.

Every Top 25 Markets saw weekday RevPAR gains except Atlanta, New Orleans, and San Diego. The two markets posting the largest weekday RevPAR gains were Las Vegas (+27.1%) and Dallas (+24.7%). Overall, 13 of the Top 25 reported double-digit weekday RevPAR growth.

The rest of the country followed a similar pattern to the Top 25 Markets but at a more subdued level with ADR the main driver of weekday RevPAR, which increased 6.7%. RevPAR on shoulder days was up 1.0%, while the weekend fell 0.8% due an occupancy decline of 2.2ppts. Taking a deeper look, weekend demand was down the most in the 50 largest markets (based on supply) after the Top 25. Those markets saw weekend demand decrease 3.4% YoY versus the remaining 92 markets, where weekend demand fell 1.9%. Some of the largest individual swings were in college football markets, where year-over-year game schedule shifts matter. However, 78% of those 50 markets saw weekend demand fall versus just over half of the remaining ones.

The weekend demand drop was due mostly to economy hotels, which were responsible for more than half of the decrease in the next 50 markets. Among the remaining markets, 63% of the weekend decline came from economy hotels. Interestingly, weekend demand was down in all types of hotels in the remaining markets, while Luxury and Upper Upscale in the next 50 markets saw rising weekend demand.

Conventions and conferences also helped boost performance, evidenced by group demand among Luxury and Upper Upscale hotels increasing 8.7% YoY (+27.4% from the previous week). Year over year, group occupancy increased 1.7ppts with the Top 25 Markets again showing the largest impact on performance. Group occupancy increased 2.5 ppts, while group occupancy for the rest of the country increased 0.7ppts.

Given the strength of groups, it’s not surprising that weekday RevPAR increased in the double-digits for Upper Upscale (+13.4%) and Upscale (+11.3%) hotels with Luxury RevPAR at +9.0%. Weekends and shoulder periods also produced strong performance for the top three hotel chains scales. Upper Midscale hotels posted respectable weekday performance (RevPAR: +6.2%), while weekends and shoulder periods were flat. Midscale hotels experienced flat weekday RevPAR and negative RevPAR change for the other two periods. Economy hotels decreased for the weekday period as well as weekends and shoulder periods.

Final thoughts

The story we have shared throughout the year has become somewhat repetitive as the industry returns to normal. Business travel continues to grow, conventions and conferences are strong, the U.S. Top 25 Markets are recovering, and leisure travel is resuming seasonal patterns. Hotels in the higher tiers are also posting the strongest performance given they were the last to recover and tend to be in the Top 25 Markets. While the news is not riveting reading, it is important to share the news that our industry is stabilizing and is expected to continue at a normal pace for the rest of the year and into 2024.

Looking ahead

In the week ending 18 November, we expect to see somewhat softer but decent midweek performance relative to the weekend with business travelers fitting in trips before the Thanksgiving holiday in the U.S. Group demand is also expected to be respectable for this time of year. Weekend performance, however, will be negative as demand normally falls 6ppts each day as people prepare for their holiday trip.

U.S. hotel occupancy will plunge the week ending 25 November due to Thanksgiving. Looking at the past 10 Thanksgivings (excluding 2020 and 2021), demand has fallen WoW by an average of 21%, resulting in a 13-percentage point drop in occupancy. ADR follows, averaging 10% less than the week prior to Thanksgiving. Altogether, RevPAR falls by nearly 30% versus the week before the holiday.

We expect that this Thanksgiving week will follow past results with occupancy near 50%. The 10-year average is 49.6% and has ranged from 45.2% in 2011 to 52% in 2018. In 2019, occupancy was 50.6%. As in past years, ADR will decrease WoW, but it should be up around 2.5% YoY. As a result, weekly RevPAR comparisons will likely remain positive despite the lower demand

This article originally appeared on STR.