-

Weekly Global Hotel Performance Trends from STR: 3 - 9 December 2023

Highlights

- U.S. ADR soared on the back of strong year-over-year growth in Miami and New York City.

- The positive side of the Art Basel calendar shift drove growth in Miami.

- New York City led the nation in absolute RevPAR.

- China posted the largest RevPAR gain, continuing a 10-week trend.

- New Year's Eve demand across the world is expected to be down slightly compared to last year due to the holiday calendar shift from Saturday to Sunday. ADR will remain strong.

U.S. performance

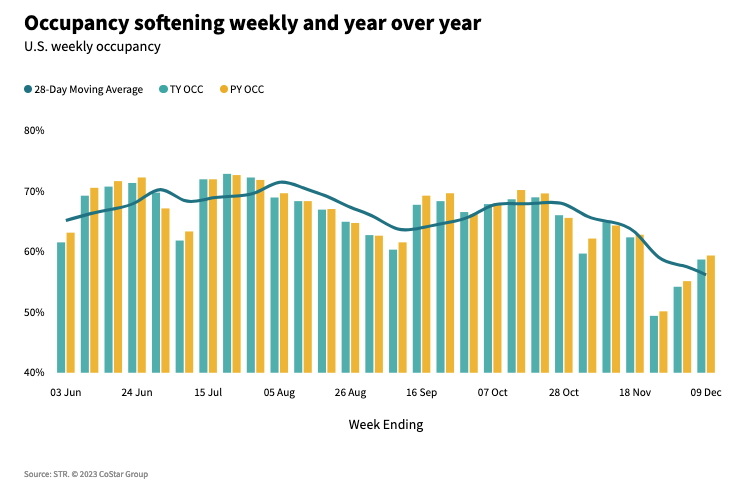

U.S. hotel occupancy reached 58.7%, up 4.5 percentage points (ppts) compared to the prior week as holiday leisure travel kicked in along with the return of end-of-year business and convention travel. Occupancy, however, was down 0.7 ppts versus last year. Average daily rate (ADR) increased 4.5% year over year (YoY), resulting in a 3.3% increase in revenue per available room (RevPAR). ADR has been driving RevPAR growth for most of 2023 even as occupancy has slipped. This is more evidence of hoteliers continuing to price with a focus on margins rather than occupancy.

Like in past weeks, the Top 25 Markets drove industry growth with RevPAR increasing 5.8% on the back of a 6.6% ADR gain. The weekend (Friday & Saturday) produced the largest RevPAR increase (+7.8%), a reversal of the pattern seen for most of the fall when weekdays (Monday-Wednesday) tended to be the strongest. Top 25 weekday RevPAR grew 5.6% with shoulder days (Sunday & Thursday) up 3.5%. In the remaining markets, RevPAR increased 0.8%, all on ADR (+2.1%) as occupancy declined 0.7ppts. Unlike for the Top 25 Markets, weekdays showed the largest RevPAR gain (+2.4) followed by shoulder days (+0.5%).

As noted in the previous week's results, Miami was expected to have a significant impact on industry performance due to the calendar shift of Art Basel. Miami RevPAR increased 67.9% YoY and accounted for nearly half of the nation's RevPAR gain, adding 140 basis points to the result. Recall, one week earlier, Miami negatively impacted the country. Art Basel 2022 began on 28 November with most of the activities taking place over the weekend. This year, the event began 4 December. When comparing this week's performance to the comparable week last year, RevPAR declined 1.8%, most likely impacted by the one-day shift in the event from Thursday-Saturday to Friday-Sunday. Miami performance in the next week of data, specifically Sunday, will benefit from this one-day shift.

In the remaining Top 25 Markets, New York City saw its second highest RevPAR of the year (the highest was seen in the week when the U.N. General Assembly met). Occupancy in the City reached 89.9%, the fourth highest level of the year. This strong performance bodes well for New York City's holiday season over the next couple weeks with New Year's Eve likely capping performance for the year.

Three other markets this week, Anaheim, Boston, and San Diego each saw RevPAR grow by 20% or more. All three markets posted increases in group occupancy. San Diego and Boston also recorded strong weekend performance with RevPAR increasing 89.0% and 59.4%, respectively.

Compared to last year, group demand in the week was essentially flat, however, the mix of weekday versus weekend and shoulder has changed. This year, weekdays produced the greatest gains, while weekends and shoulders declined slightly, reflecting the changing mix of group business with more business and less leisure compared to last year.

The top hotel classes (Luxury, Upper Upscale & Upscale) dominated the industry's RevPAR growth with all three recording ADR and RevPAR increases above 4%. Occupancy for all three was north of 65%. RevPAR in Upper Midscale segment was up 0.7%, while Midscale hotels fell 1.1%. Economy hotels continued to see falling RevPAR, dropping by 3.3%, which was the smallest decline of the past five weeks.

Global hotel performance

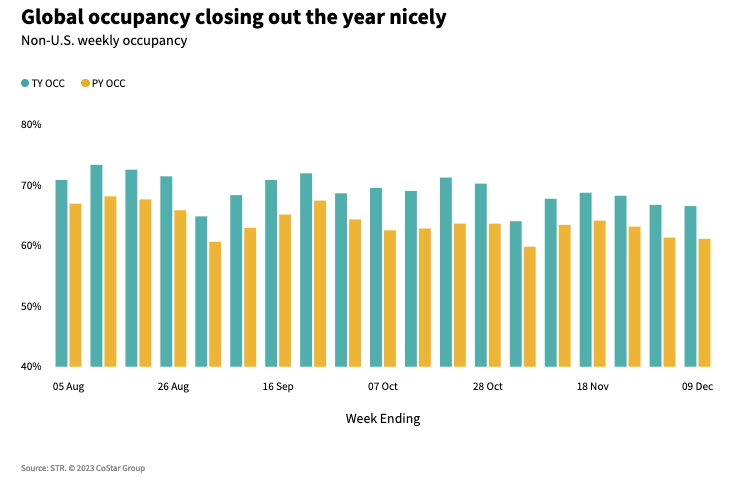

Global occupancy, excluding the U.S., moved to 66.5%, up 5.3ppts YoY and flat from the previous week. Occupancy is trending in line with pre-pandemic norms as 2017, 2018 and 2019 all showed a similar slowdown of occupancy from mid-November toward the end of the year. Global ADR (US$130) increased 7.9% with RevPAR (US$87) growing 17.3% YoY; double-digit RevPAR growth has been the norm all year long, but the magnitude is trending down and has been in the high teens for the past seven weeks. The summer led to growth in the low-to-mid 20s.

Among the top 10 countries, based on supply, occupancy nearly mirrored the globe with the measure up 6.9ppts YoY to 66.9%. Occupancy is nearing pre-pandemic levels as the same week in 2019 reached 67.6% and 2017 (which matches 2023 day for day) was 69.9%. Top 10 ADR (US$116) grew 7.4% with RevPAR (US$78) rising 19.7% YoY.Ê

Italy, which led the European contingent of the Top 10 countries during the summer (May-August) with RevPAR growth of 18.1%, is now seeing some softening. In the most recent week, the country saw RevPAR increase 10.3% on an occupancy gain of 3.7ppts with ADR growing 3.1%.ÊThere was significant variation in the country with RevPAR in Tuscany down 31% but up 36.4% in Basilicata/Calabria/Puglia.

As it has for the past 10 weeks, China had the largest RevPAR gain of the top 10 countries with the measure rising 53.7%.Ê

Looking ahead

We anticipate ADR to remain strong for the rest of the year despite waning demand ahead of the holidays. Outside the U.S., performance remains robust as countries continue to recover. However, growth rates are beginning to moderate and will likely return to normal levels early next year.

Around the world, we expect demand to wane as the end of year approaches.

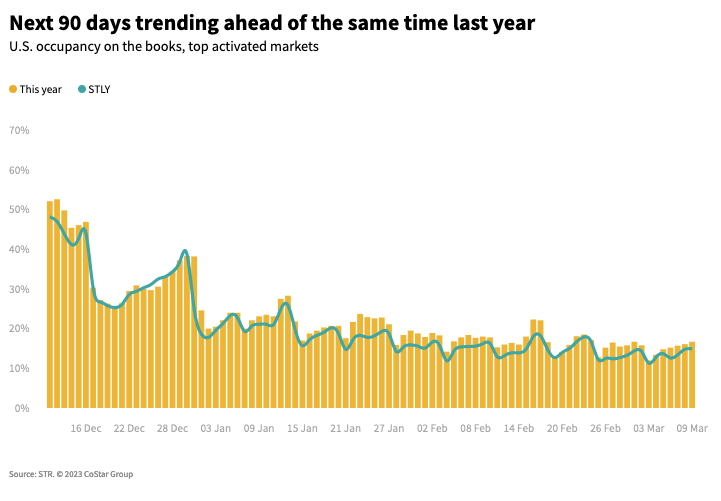

We also expect New Year's Eve to be slightly softer than last year due to the calendar shift from Saturday to Sunday with ADR remaining strong. As the new year begins, occupancy on the books in the top U.S. markets is trending ahead of last year, indicating a strong start to 2024.

This article originally appeared on STR.