-

Weekly Global Hotel Performance Trends from STR: 18 - 24 June 2023

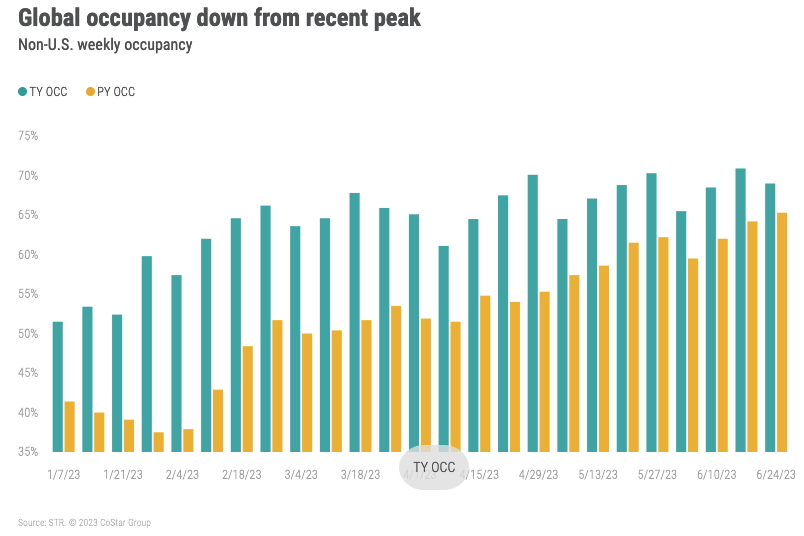

Global Performance

Global occupancy (excluding the U.S) was 69.0%, down slightly from last week’s post-pandemic high of 70.9%. Despite the week-on-week decrease, occupancy continued to strengthen, up 3.7ppts YoY. Nominal ADR was up 21.1% from the comparable week last year to US$163, resulting in RevPAR US$112, up 28.0% YoY, a post-pandemic high.

Among the top 10 countries, based on supply, occupancy increased 3.5ppts YoY to 70.5%, also down from last week’s post-pandemic high. ADR for the top 10 countries grew 20.5% YoY to US$160 with RevPAR increasing to US$113 (+26.8% YoY). All key countries saw positive RevPAR comparisons except Germany and Mexico.

- As it has for the past six weeks, the United Kingdom continued to lead the top 10 in occupancy with a level of 84.0%, up 2.5ppts from a year ago. ADR also grew a strong 11.2% YoY.

- RevPAR in France increased 49.0% YoY on strong ADR and occupancy gains.

- China’s RevPAR was up 42.6% with an occupancy gain of 4.5ppts along with a 32% ADR increase.

Outside of the Top 10, destinations known well for leisure and holidays posted the highest occupancy again as they have for the past four weeks. Countries included were Ireland 90.2% (+3.1ppts YoY), Greece 87.7% (+4.6ppts), Malta 86.8% (+20.3 ppts) and Fiji 86.3% (+6.2ppts).

U.S. Performance

One week into summer (officially), U.S. occupancy rose to 71.4%, up 0.6 percentage points (ppts) from the previous week but down 0.7ppts from last year. Average daily rate (ADR) grew 0.9% year over year (YoY) to US$159. Revenue per available room (RevPAR) stayed essentially flat YoY (-0.1) at US$114, due to the slight drop in occupancy.

This modest performance compared to the same week last year is a continuation of a trend seen over the past several weeks. An increase in Americans traveling abroad in 2023 is impacting domestic performance, and there are fewer international travelers coming to the U.S to make up the difference. However, room demand for the week wasn’t too bad as it was the fourth highest for this particular week over the past 23 years.

Day-of-week shifts happened in part due to the recently declared U.S. holiday, Juneteenth, which fell on Monday, 19 June. Due to the pandemic and the newness of the holiday, which received federal status in 2021, this holiday had a minimal impact on travel until this year. Across all markets, Monday occupancy of 64.3% decreased 1.2% week over week.

Historically when a Monday holiday occurs, business travelers stay home, and company group events are pushed to later in the week or a different week. On the flip side, Monday holidays drive increased leisure travel as people take advantage of a three-day weekend that enables more travel. The change in this business/leisure travel dynamic can been seen in the performance of the Top 25 Markets (where business travel plays a larger role), especially on weekdays.

- As compared to last year, Monday occupancy fell the most (-2.3ppts) with Sunday

(-1.2ppts), Tuesday (-1.0ppts) and Wednesday (-0.8ppts) also showing declines. - Thursday (-0.2ppts) and Friday (-0.1ppts) occupancy were slightly down whereas Saturday (+0.3ppts) was up.

- ADR increased 0.4% for the week. Days with the greatest occupancy declines also produced the greatest ADR declines with Monday reflecting the largest decrease at -2.2%. Saturday and Friday produced the greatest increases of +2.2% and +1.0%, respectively.

For the rest of the U.S., weekly occupancy was down 0.7ppts YoY, the same rate as the Top 25 Markets but with some notable differences:

- Monday occupancy was down much less than the Top 25 (-0.7 YoY) with Wednesday (-0.6ppts) and Thursday (-0.9ppts) also down less than the Top 25.

- Sunday and Tuesday showed the smallest declines (-0.1ppts and -0.2ppts, respectively).

- Friday and Saturday reflected the greatest YoY occupancy declines of -1.4ppts and -1.2ppts, respectively. This is consistent with what we have seen recently as these markets saw strong pent-up demand a year ago.

- ADR for non-Top 25 Markets increased 1.3% as compared to +0.4% for the Top 25. Tuesday and Wednesday showed ADR increases of +2.0% or more. Consistent with the softer occupancy, Friday and Saturday ADR produced minimal increases of +0.5% and +0.3%, respectively.

Gatlinburg had the nation’s highest weekly occupancy (86.0%) followed by Alaska (85.2%) and New York City (84.7%). Other markets seeing solid occupancy included Omaha (82.0%), host of the NCAA Baseball World Series.

Concerts, sports, Pride events and Juneteenth celebrations boosted performance across many markets, especially over the weekend. The Top 25 saw weekend occupancy of 82.8% with Denver and Minneapolis, which hosted Taylor Swift’s Eras tour, posting their highest weekend occupancy post-pandemic. Portland OR, hosting a Formula E racing event at Portland International Raceway (think Formula1 racing with electric cars) reached its highest weekend occupancy since the pandemic of 85.5%. Almost half of all markets across the U.S. saw weekend occupancy above 80%.

Group demand is softening as expected now that school is out, and vacation season has begun in earnest. Additionally, the Juneteenth holiday also had an impact on groups. Group demand among Luxury and Upper Upscale hotels decreased compared to last year’s levels by 4.3% and dropped 3.6% from the week prior.

Final thoughts

U.S. occupancy continued to grow as summer builds although the metric has fallen short of last year’s level for the past four weeks. The Juneteenth holiday led to weaker business and group travel. Other challenges include changes in travel patterns, from resorts to Top 25 Markets and/or international outbound. Concerts, sporting events and festivals are driving demand, making it the era of epic events. ADR is softening, which is not surprising given the changes in demand from pure leisure to a more normal mix of business transient, group, and leisure. Outside of the U.S., the recovery remained in full swing.

Looking ahead

For the week ending 1 July, U.S. occupancy is expected to rise slightly before dropping in the week ending 8 July. As seen in STR’s Forward STAR data, this summer is poised to resemble last summer, however, ADR growth is likely to remain somewhat muted and is anticipated to fall week over week for the next two weeks. As a result, RevPAR is anticipated to be flat to slightly down as compared to last year. Global performance, excluding the U.S., will see healthy growth over the next several weeks.

This article originally appeared on STR.