Excerpt from HVS

While the impacts of the COVID-19 pandemic on the lodging industry are ongoing, this tenth annual HVS Lodging Tax Study quantifies the revenue impact of the pandemic over the past year. An analysis of 25 major US markets shows losses totaling approximately $1.3 billion in 2020 from historical levels in 2019. HVS forecasts a loss of $1.45 billion in rooms revenue in 2021 from a baseline scenario with no pandemic. HVS also provides historical data on tax rates and the collection and distribution of revenue from lodging taxes levied in all 50 States and the 150 largest US cities.

Introduction

Lodging taxes provide a critical source of support for the convention and tourism industries. Lodging tax revenues fund debt service for the construction of convention centers, arenas, and other public assembly facilities. This revenue source provides a large share of the funding for destination marketing organizations (“DMOs”) and covers the operating deficits of convention center venues. Beginning in March 2020, the United States hospitality industry faced unprecedent challenges and losses resulting from the COVID-19 pandemic. The lack of convention business, leisure, and business travel across the country during the early days of the pandemic severely reduced lodging tax revenue streams.

Despite the rapid deployment of a readily available vaccine, vaccine hesitancy and more virulent strains of the SARS-CoV-2 coronavirus have created more uncertainty about the pace of economic recovery of the hospitality industry. This report provides insight into how the COVID-19 pandemic reduced lodging tax revenues by analyzing available historical data on lodging tax collections. Using one year of historical data, HVS quantified the impact of the virus and projected the extent of ongoing the economic fallout from the pandemic, which may last for years. Future editions of the HVS Lodging Tax Study will track how the situation evolves.

COVID-19 Impact on the Lodging Industry

The hospitality and tourism industries have proven to be the most vulnerable industries to the COVID-19 pandemic with percentages of revenue losses far exceeding that of the overall economy. As of January 2021, U.S. Travel Association and Tourism Economics reported approximately $500 billion in losses and $64 billion in lost federal, state, and local taxes by the end of 2020.

The hospitality industry relied on direct relief offered throughout the COVID-19 pandemic, including the March 2020 $2.0-trillion CARES economic-aid package, the December 2020 $900-million aid package, and the March 2021 $1.9-trillion American Rescue Plan. The $3.5 trillion budget resolution currently working its way through the congressional approval process promises additional economic stimulus. Full recovery from the initial shock of the COVID-19 pandemic, according to the American Hotel & Lodging Association is not expected until 2024, with state and local tax revenues generated by hotels recovering earlier, albeit in 2023.

Lodging Tax Loss Forecast

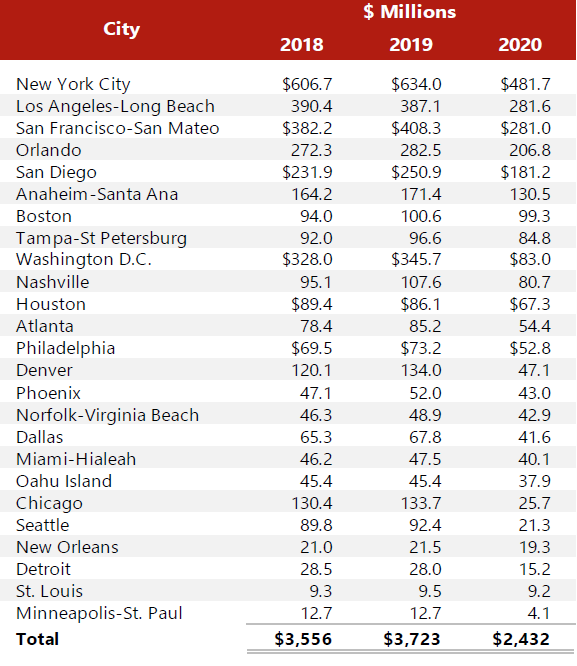

HVS combined data on lodging tax collections with projections of the performance of hotel markets in 25 major US cities. Before the onset of the crisis, during fiscal year 2019, 25 major US markets generated approximately $3.7 billion in lodging tax revenue as shown in the figure below. In total, these markets experienced a -34.66% decline in revenues from 2019 to 2020.

Lodging Tax Revenues in 25 U.S. Markets

{kind=link}

Source: HVS

The performance of the 25 markets during prior economic shocks provides an indication of how recovery from the COVID-19 pandemic may play out. Urban markets that relied heavily on meetings and groups and individual business travel to generate room night demand have been more severely depressed by the pandemic than markets that rely on leisure demand. Long-haul air access and international markets have also been affected more than drive-to markets.

Given the uncertainty surrounding the pandemic throughout 2020, economists and analysts relied on the shape and magnitude of prior economic shocks to estimate losses resulting from COVID-19. These estimates varied from the less-severe (V-shaped recessions similar to the recessions of the 1990s and early 2000s) to the more-severe (U-shaped recessions like the Great Recession or, under the worst-case scenario, an L-shaped recession like Japan experienced in the 1990s). Following the nadir in 2020, recovery in occupancy, average daily room rate (“ADR”), and revenue per available room (“RevPAR”) show recovery patterns resembling that of a V-shaped recession.

Click here to read complete article at HVS.